Updated April 27, 2022

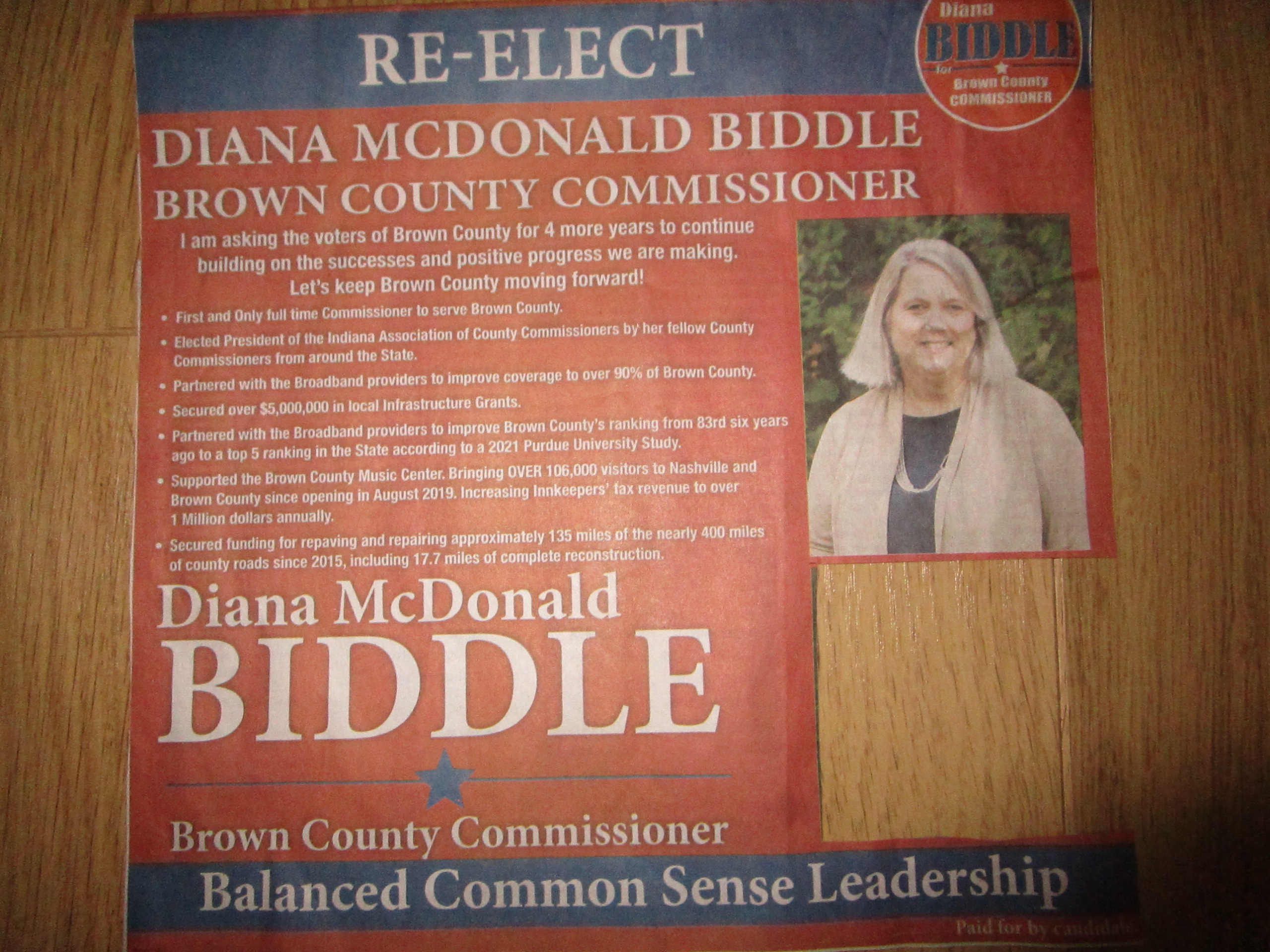

“Houston” – oops – Brown Countians – Do we have a problem? In a political advertisement (paid for by the candidate) in the April 20, 2022, Democrat, Commissioner Biddle (aka Diana “McDonald” Biddle) claimed she is the “First and Only full-time Commissioner to serve Brown County.” The other commissioners are Jerry Pittman (President) and Chuck Braden (Vice-President).

Do we need “a full-time commissioner” or someone that needs to work full time to meet the needs of a part-time position? Despite what candidate Biddle considers full-time, we have two other commissioners. Further, the county also uses expensive consultants and advisors to provide the needed expertise and services. What are the contributions of the other two commissioners?

Do claims of individual accomplishments for group efforts where the facts do not support the level of individual contribution, undermine a candidate’s credibility? Does it also undermine and diminish the contributions of others – including the other commissioners, volunteers, and government personnel?

Alleged accomplishments include taking credit for receiving the funding from state and federal policies related to broadband, federal stimulus, covid-related grants, and highway funding.

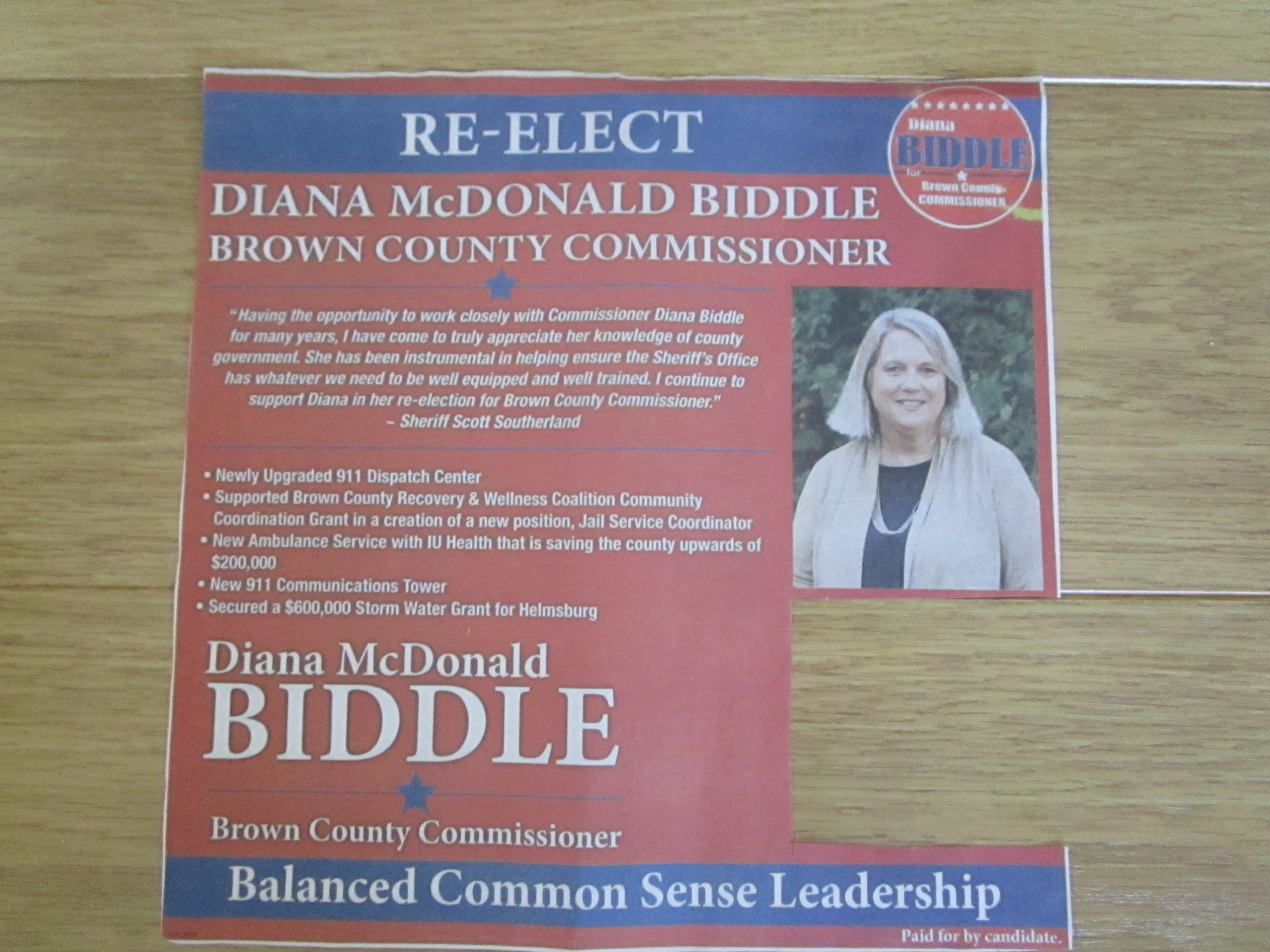

Another advertisement in the April 26, 2022 edition of the Democrat repeats the overstated accomplishments (ambulance contract for example).

In the case of the Brown County Music Center (BCMC), despite a commitment by candidate Biddle and the other elected officials that county taxpayer money would not be used to fund the BCMC, she personally engineered- without the knowledge of the council, a $239,000 subsidy – some of which included rent. No itemized list of what taxpayers received was ever provided.

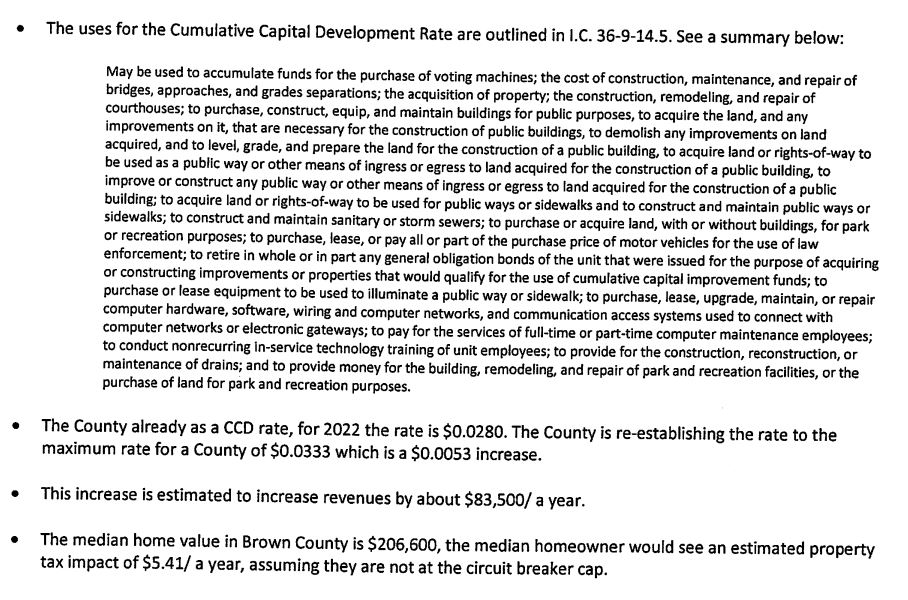

-

- Brown County Democrat. GUEST OPINION: What’s been happening with your county’s finances by Kevin Fleming. Includes the details regarding the lack of transparency and oversight of Commissioner Biddle’s actions regarding the $239,000 “Rent” payment to the BCMC. Commissioner Biddle also serves on the Music Center’s management group.

- “I asked commissioner Biddle if the payment amount also included insurance premiums as indicated in the MOU. Her answer was that “It’s for any expenditures the music center might need it for.” That describes the $239,000 payment unequivocally as a subsidy for the music center, not a rent payment.”

I encourage voters to ask for documentation that supports candidate Biddle’s claims of accomplishments. One source would be the minutes from commissioner’s meetings. Articles in the Democrat would be another source but too often repeat the claims being made without the factual back-up.

Individual Hubris and Abuse of Power. Political advertising and promotions are expected to influence “perceptions.” They also can overstate or grossly exaggerate individual accomplishments and capabilities. It is a fact of human nature that some individuals seek power, power is addicting, and always corrupts to the detriment of those being served. The vote is the one way to support “term limits” to help avoid the unnecessary accumulation and abuse of power.

Compensation and Benefits. The commissioner is a part-time position that pays around $17,000 (2021). This compensation does not include the value of the county health insurance benefit that was voted in and is available to the council as well as commissioners.

The out-of-control health insurance spending was first addressed in 2016/2017 by the previous auditor. The county has recently selected a new vendor and supplier that has finally reduced costs. The leadership in the schools successfully addressed their rising costs and budget deficits in 2017. Their change has resulted in documented savings.

Ambulance Contract. Commissioners signed an agreement with Columbus Regional. Costs exceeded budget (2018-2021) to the total amount estimated at over 300K which included an overlap because of the effective date of the new contract. An extra million (Capital Improvement Loan) was borrowed to help cover the expenses and the new contract is with IU Health.

-

- Apr 14, 2021. County contracts with different ambulance provider

- The county had a net-zero contract with CRH, which meant CRH billed the county for any ambulance costs not covered by health insurance. For 2019, the county paid more than $600,000. The commissioners budgeted $515,000 for 2020 to pay the contract for 2019. Making up that difference required the county to find more money

- Biddle said last week that the $540,000 annual payment to IU Health Lifeline was saving the county around $200,000. …. “That is a fixed number. We don’t have to guess on what it might be. We can plug that number in and then we don’t have to come up with any more money,” she said.

- “Savings.” Similar to Health Insurance, the county was overpaying for services.

- Feb 17, 2021. COUNTY NEWS: Ambulance contract update

- July 7, 2019. COUNTY NEWS: More money needed to pay ambulance contract

- The total bill for ambulance service in 2018 was $547,540. Biddle said she paid CRH $440,196. On July 15, the council was asked to approve transferring $107,344 to pay the remainder of the contract.

- Biddle said the increase is a result of a change in the Medicaid billing reimbursement. “There was a loophole in some new rule that was created with Medicaid that allowed them to get a larger reimbursement. They closed that loophole,” Biddle said. Source (documentation) supporting this statement? What was required in the contract?

Quality of Decision-Making. I have routinely attended commissioner meetings for years. This “full-time” status has supported decisions that lead to higher costs and poorer quality. Too often, it appears decisions are made before the issues are discussed at a meeting. Input and questions from citizens are ignored.

The operating principle reinforced by candidate Biddle is “Spend, Tax, Borrow.” The indirect effects of a “full-time” commissioner can result in the hands-off approach embraced by the other two commissioners that with few exceptions, just go along with her decisions without question or debate. Does she feel she has to work “full-time” because the other two are not capable of contributing to the workload?

Commissioner Meetings. Commissioners’ meetings are longer than necessary and key issues that lead to decisions too often lack the documentation to support the decision. Meetings are recorded but any supporting detail (if available) is not available on the website. The School Board offers a good example for conducting meetings in a professional manner and decisions are supported with facts and data. Unlike the county, information regarding policy changes and spending are discussed in previous meetings and questions “are” addressed by those knowledgeable of the issues.

County Gentrification? Development through the expansion of sewers (unneeded in many if not most cases), is a priority of the core of the local republican party and their candidates including candidate Biddle. Development can benefit the few at the expense of the many. A higher cost of living due to unneeded sewer hook-up fees and monthly bills contribute to gentrification where those in the low to moderate income levels are replaced by the more affluent citizens.

Transparency and Decision-Making. A deliberate lack of transparency and embracing an ignorance-based decision-making strategy supports the agenda of the few at the expense of the many. Such an approach is believed to offer plausible deniability when decisions result in bad outcomes.

Honesty and Integrity. Statements made by the commissioners can rarely be taken at face value. Commissioners rely on anecdotes, assumptions, hearsay, and lack of facts and data as a basis for too many of their decisions. A recent example of this approach was represented at the meeting where the Brown County Regional Sewer District (BCRSD) was granted $300,000 without a project plan. In 2018, the BCRSD was granted $270,000 of taxpayer funds to support a new sewer plant in Bean Blossom. They spent $220,000 and was not able to acquire land. They now have another 300K which was approved by the commissioners and council without a project plan, discussion, or identification of risks.

Candidate Biddle’s actions have contributed to a system of corruption that in a moral sense, leads people working in this system to develop an inability to distinguish right from wrong – to recognize truth. The classic example is ignoring the requests for information from the public that require little time to provide but requires intervention from the State to obtain.

Lack of transparency also contributes to corruption. Claims of accomplishments where the facts do not support the level of individual contributions also undermine credibility, confidence and trust in county government and the support of those that contributed to the solutions. On broadband, volunteers and town officials have worked this issue for years and the influx of state and federal money supports the needed access.

Citizens Denied Input at Commissioner Meetings. The ultimate example of a corrupt system is the policy agreed to by all the commissioners and supported by the local Republican party, to not allow citizens to ask questions at their meetings. This policy is being ignored by the citizens.

Satirically speaking, this gag order on citizens does make sense. Why waste time listening to people whose input you are going to ignore anyway? And further, if major decisions can be made before the meetings, why have meetings at all, or elections for that matter? Wouldn’t that be nice?

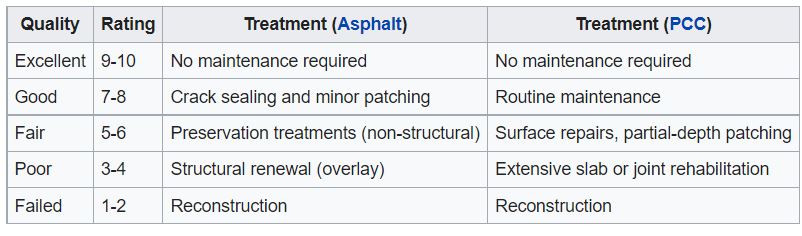

Roads and Bridges. The status on roads and bridges can be supported through a published plan. Posting this plan and current updates on the highway department website (a new and welcomed improvement) can keep citizens informed of the plan, status, and accomplishments. Additional information explaining how roads are selected for repairs and paving would also be an improvement.

Road and Trail Closing. With little deliberation or research, candidate Biddle led the decision to close the Railroad Crossing on Indian Hill Road without allowing any input from the residents that would be affected. This decision also resulted in closing a portion of the Tecumseh Trail.

The Tecumseh Trail was closed from State Road 45 to the parking area south of Beanblossom Creek.

Overlook – Clear-Cutting. Candidate Biddle’s lack of oversight and leadership also contributed to the clear-cutting at the overlook. She led the successful logging on the west side of the overlook and failed to ensure the same standards were applied on the east side.

Lack of Capital Improvement Planning. The deliberate lack of a capital improvement plan and budget further contributes to waste and poor quality of decision-making. Such a plan would identify funding requirements for infrastructure repairs and replacements. However, such a plan would identify funding needs that would compete with other projects that she may independently feel is more important. This leads to ensuring we maintain the habit of borrowing the money for infrastructure projects that can also be used to cover operating expenses that have exceeded the budget.

The findings from the recent audit for 2019 and 2020 by the State Board of Accounts (SBOA) is another indicator of systems and processes that do not contribute to the effective and efficient use of tax dollars. Incapable systems can contribute to waste that can exceed 20% of budget.

Power and Monopolies Corrupt. As mentioned previously, it is a fact of human nature that individuals and groups seek power, power is addicting, and always corrupts to the detriment of those being served. A one-party monopoly on political power also contributes to corruption. This monopoly along with name recognition can be enough to guarantee an individual an elected job for life. Monopolies – including political ones, always lead to poor quality of services and higher costs.

In a monopoly, the interest of the few takes precedent over a decision that leads to outcomes where everyone benefits, or at least, is not any worse off in the long-term. This goal can be accomplished through the application of better methods and tools.

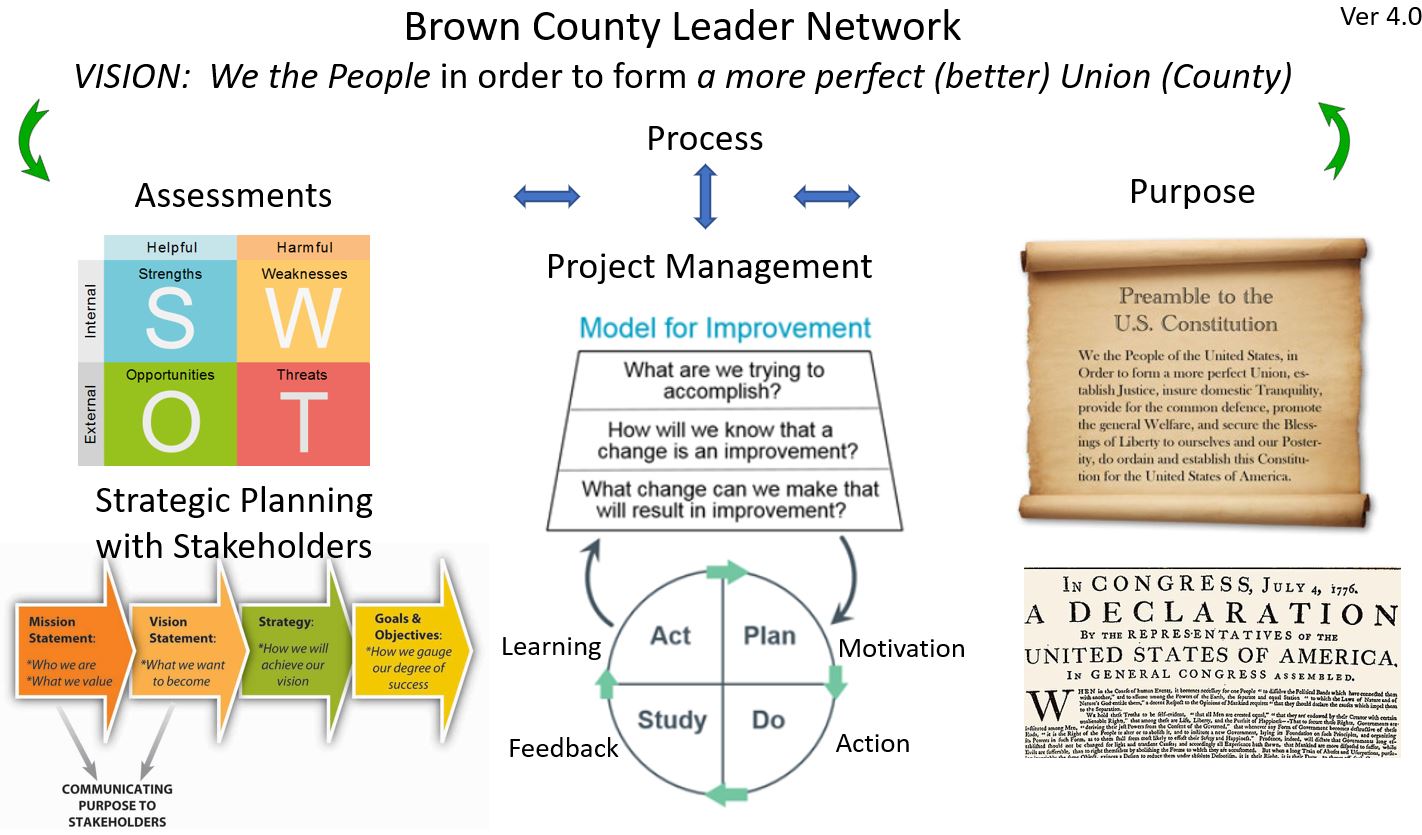

Ironically, Commissioners Biddle and Pittman supported applying for a grant that led to the development of the Brown County Leader Network. The BCLN includes methods and tools that support analysis, planning, and better decision-making that can produce higher quality results. Commissioners have expressed no interest in learning more about the proven methods that would support improvement and transparency. The approach supports citizens and not the special interests that are represented by the monopoly.

Primary Vote. The competitive opponent for candidate Biddle in the Republican primary is Ron Sanders. He also opposed her in 2020 and came within 489 votes of winning.

Cross-Over Votes. In Indiana, those that have voted Democrat can ask for a Republican ballot in the primary. If candidate Sanders wins the Republican primary, the general election will be between him and Stephanie i.e., Kritzer (D). The other options can be candidates that run as Independents.

Conclusion. Do we need someone who believes she must work full-time to accomplish the requirements of a part-time position? Three competent part-time commissioners are sufficient and if not, better candidates are needed.

In America (see Constitution), “We the People” are top management and are responsible for improving our system of government. In addition to new leadership, citizens can support and expect the application of proven methods and tools introduced through the Brown County Leader network (BCLN). The application of the better methods can result in the needed changes to the system and result in outcomes where everyone can benefit and not just the special interests represented by candidate Biddle.

Roads and Bridges. The condition of roads and bridges probably gets the most complaints in social media comments. The highway superintendent briefs the Commissioners at every meeting (two a month). Occasionally, a citizen or two will provide a complaint at the meetings and rarely gets a satisfying response.

Roads and Bridges. The condition of roads and bridges probably gets the most complaints in social media comments. The highway superintendent briefs the Commissioners at every meeting (two a month). Occasionally, a citizen or two will provide a complaint at the meetings and rarely gets a satisfying response.