Pay and Benefits. the County Council has recognized the need to re-examine the employee compensation system to include salaries, grades, positions, benefits, et.al. It has been incremented over time with a series of “patches” and has created conditions that are not being perceived as being fair and equitable. And given the constraints on the county’s ability to raise taxes, makes for an interesting challenge. What has been missing in past change efforts to include requests for higher grades and new positions, has been a workload analysis linked to statutes, combined with an assessment of performance.

New Position – Commissioner Assistant at 42K a year. Commissioners (Wolpert, Pittman) pleaded that their part-time assistant position be converted to full-time so they can post the new position immediately. The current part-time position will remain for the rest of the year and the new position is to be immediately advertised. I do not recall that the commissioners had a vote on adding the full-time position – assume this will happen at this Wednesday’s meeting.

Vote to Approve. After about a 90-minute discussion, the council voted to approve – 4 Yes (Hewett, Rudd, Kemp, Kirby), 2 No’s (Byrd, Swift-Powdrill), and 1 abstain (Redding). No discussion or details were presented as to the workload (the need). What is the current workload of the commissioners and how is this distributed among the three commissioners?

Need? The need for a full-time position emerged during the last few weeks with the appointment of Blake Wolpert. Commissioners (Wolpert, Pittman) voted to contract with a former employee that served in the full-time admin assistant role, to help with their budget. Last fall (post-election) commissioners and council decided to re-structure the position to part-time and then create a new full-time HR director.

On-the-Job Training. When new council and commissioners are elected, I do not recall any that could hit the ground running. Some candidates generally show up for a few meetings to get a feel for the position which is not exactly good preparation. And state statutes, along with the lack of SOPs, do not make learning about county operations, finance and budgeting an easy endeavor. At a minimum, prospective candidates should review about 2-3 years of minutes of meetings to identify their tasks and responsibilities. A review of the statutes identifying the requirements of the elected office would also be of value.

Budget. The Circuit Court needed another 6K to pay for psychiatric services that are needed to assess the defendant’s ability to stand trial. This expense varies – $4,600 last year and 1$1K in 2021. The Coroner needed another $18,500 for autopsy services.

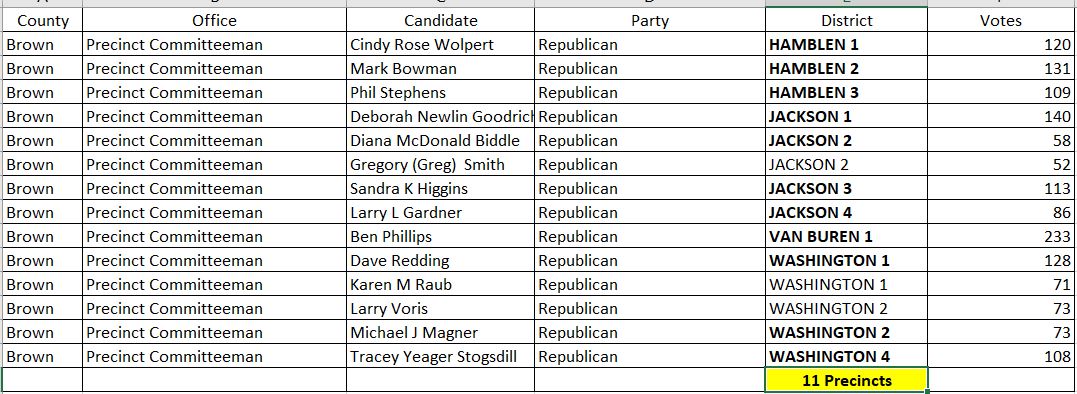

Phil Stephens Hamblen 3 (Hamblen Township Trustee, Director, Brown County Recycling.)

Deborah Goodrich, Jackson 1

Diana Biddle, Jackson 2, (Replaced by Sandy Higgins).

Duane Parsons, Jackson 3,

Larry Gardner, Jackson 4,

Jim Kemp for Van Buren 1, (Councilman, Treasurer)

Ted Adams, Washington 1, (Prosecutor)

Theresa Cobian, for Washington 2 (Commissioner Assistant)

Washington 3 (vacant).

Disclosure: I register as a Republican in the primaries and do not always vote a straight party ticket.

Comments from the Chair of Brown County Republican party on straight-ticket voting: “Even as a party chairman, Bowman said he doesn’t like to see so many voters choosing the straight-party option. To him, that shows voters lack knowledge about the candidates. The choice listed from one’s own party isn’t always automatically the best choice for the job, he said.” BCD GOP SWEEP Nov 14, 2018

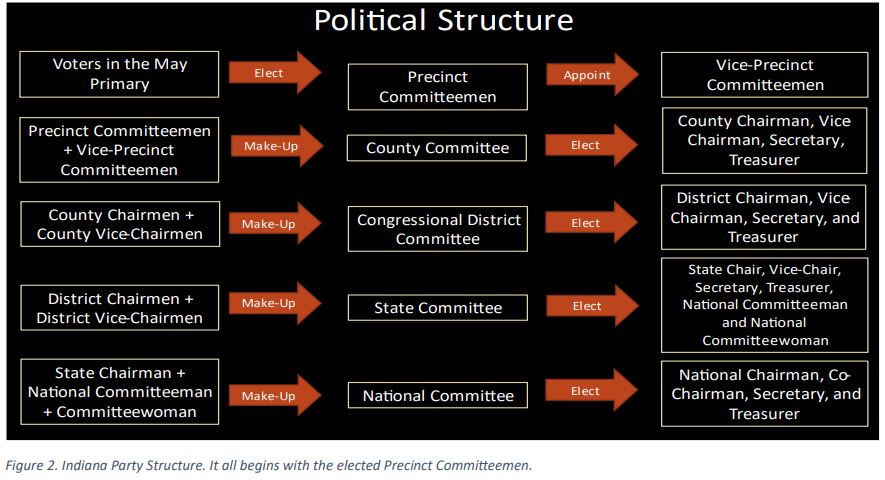

Precinct Chairs and Vice Chairs elect the local GOP Chair. This leadership group influences the selection of local candidates for offices and appointments. They also determine the direction of the county which includes a bias for development not supported by the community.

One of the strategies supporting development is the expansion of sewer service throughout the county. “Appointed” officials of the Brown County Regional Sewer District (BCRSD) Board contracted for the development of a “county-wide” wastewater strategic plan. This plan was funded with tax dollars at a cost of over $100K. It was developed without any input from the public nor was it ever introduced at any public meetings. This plan led to a request for funding of over $50 million dollars. This overall strategy had/has the approval of the local GOP, commissioners, and council. Ref: BCRSD Sewer Expansion Project on “Trial” – For The Record

“Elephant” in the local GOP Room? The core leadership in the party includes the Bowmans. The Bowmans are owners of a real estate company and have demonstrated a bias for development. I cannot recall being at any government meetings where they did not support any kind of development-related project.

The overall situation is reminiscent of the television series Yelllowstone starring Kevin Costner as John Dutton. In the series, developers have identified how they can transition a beautiful landscape into a commercial mecca. They are being opposed by the Duttons who want to retain the beauty of the landscape and retain the rural culture.

In Brown County, it is the residents who choose to live here or retire here that provide the major source of tax revenue. Gentrification and a Gatlinburg-Lite may be the desired future of some but certainly not the majority. For instance, tourism accounts for about 12 million in taxable wages. The total taxable wages in the county from all residents is over 424 million. Brown County is considered a naturally occurring retirement community (NORC) and by Ball State economists as a “bedroom community” e.g., people choose to live here but generate their income outside the county.

Officers – Pre-May Primary Any other county positions in parentheses

Mark Bowman, Chair

Deborah Noe, Vice Chair

New: Melissa (Stinson) Waddell, Secretary and County Commissioner Assistant

Julia Reeves, Treasurer (Auditor)

Precinct chairs and Vice Chairs Any other county positions in parentheses

Hamblen 1: Cynthia Rose Wolpert (Health Board) / Blake Wolpert (commissioner as of May 2023)

Hamblen 2: Mark Bowman (local GOP Chair)/ Tanner Bowman (former paid county intern)

Hamblen 3: Phil Stephens (Director, Recycling Center) / Deborah Noe

Jackson 1: Deborah Goodrich / Darren Byrd (councilman)

Jackson 2: Diana McDonald Biddle (former commissioner) / Scott Rudd (councilman)

Jackson 3: Sandy Higgins (Jackson Township Trustee) / Jamie Voils

Jackson 4: Larry Gardner / Herb Ross

Washington 1: Dave Redding (councilman) / Keith Baker

Washington 2: Mike Magner (Highway Superintendant) / Brandon Magner (Washington Township Trustee)

Washington 3: Ted Adams (Prosecutor) / Robyn Rosenberg Bowman (PTABOA Board, Maple Leaf (Music Center) Building Corp board member)

Van Buren: Ben Phillips (Brown County Water Board member) / Brad Stogsdill (Sheriff)

Monopoly on Power. Brown County has a one-party monopoly on political power. The surveyor is the only office held by a non-GOP candidate. Centralization of power is never a good thing and leads to moral corruption and an abuse of power.

A monopoly also represents a “closed system” where input from those outside the system can be ignored and where the few can dictate the solutions for the many. A closed system is the least effective. The antidotes include transparency which would include at a minimum, complying with open meeting laws and posting meeting agendas, minutes, and audio of government meetings.

Wolpert was elected commissioner in 2004. During his tenure, Commissioners created Fire Districts that were opposed by the VFDs and others. Legal action was taken to reverse the decision that required intervention by the Indiana Supreme Court.

One of the first actions taken by Commissioner Wolpert was to add a new full-time commissioner assistant position. This action led to significant challenges and criticisms but was eventually approved. A contract was developed to provide assistance pending a selection for the vacancy. More info at the following post: County Operations and Assessments

Beginning with the March 23, 2022, meeting, Commissioners, with the support of the local GOP leadership, attempted to establish a policy restricting citizen questions at meetings. This decision was ignored by the citizens, and the policy was revoked by the commissioners.

2022 Convention Delegates – Mark Bowman, Cindi Wolpert, Blake Wolpert, Ben Phillips, Robyn Rosenberg Bowman (replacement for Chad Williams), Tanner Bowman (replacement for Diana Biddle.

There are 11 Precincts in the county –May 2020 Primary Election Results (Election winners received an average of 188 votes – from 58 (lowest) to 233 (highest).

“Voters in the May Primary elect precinct committeemen”

When you became a Republican Precinct Committeeman/woman, you took on a vital leadership role to advance Republican principles of:

Lower taxes, Smaller government, Fiscal responsibility, Individual freedom, Strong national defense, Job creation, Family values

Other

Liberty Defense: We promote safeguarding your freedoms and preserving traditional family values. We defend all Indiana residents by keeping a watchful eye on those who represent you at the Statehouse.

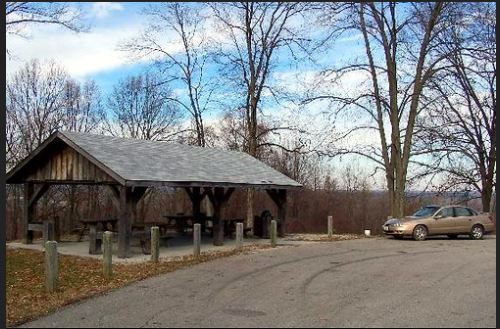

The Bean Blossom Overlook was on INDOT property. INDOT removed the Shelter due to safety concerns. The county now owns the property and a new shelter can be built.

Aug 4, 2023. The Parks and Rec board agreed to take the lead in building a new Shelter at the site. It is hoped that grants, and donations, including material and time will help keep the cost low. The County will continue to mow grass and provide insurance. Transferring the property from the county to Park and Rec was not needed.

July 19, 2023. Commissioners Pittman, and Wolpert, approved transferring the overlook property from the county to Parks and Rec with the caveat that the Parks and Rec Board would accept the property and would be interested in building a new shelter. The assumption being grants and donations would fund the project.

If you’ve driven past the Bean Blossom Overlook on State Road 135 North recently, you may have noticed a few changes: An actual view, with more cars and motorcycles stopping to take it all in.

In February, trees were cut to restore the site to the way it was more than 80 years ago — more overlook than forest. Visitors and residents alike have noticed, stopping to take photos, paint or enjoy a picnic.

The overlook was first established in the early 1930s when State Road 135 North was built. At that time, there were no trees to block the view from the first shelterhouse, which was just below the current shelterhouse.

Report on the Audit of the Financial Statement – Adverse and Unmodified Opinions

We have audited the accompanying financial statement of Brown County (County), which comprises the financial position and results of operations as of and for the year ended December 31, 2022, and the related notes to the financial statement as listed in the Table of Contents.

Adverse Opinion on U.S. Generally Accepted Accounting Principles

In our opinion, because of the significance of the matter discussed in the Basis for Adverse and Unmodified Opinions section of our report, the financial statement referred to above does not present fairly, the financial position and results of operations of the County as of and for the year ended December 31, 2022, in accordance with accounting principles generally accepted in the United States of America.

Opinion on Regulatory Basis of Accounting

In our opinion, the accompanying financial statement referred to above presents fairly, in all material respects, the respective financial position and results of operations of the County, as of and for the year ended December 31, 2022, in accordance with the financial reporting provisions of the Indiana State Board of Accounts described in Note 1.

The purpose of this report is solely to describe the scope of our testing of internal control and

compliance and the results of that testing, and not to provide an opinion on the effectiveness of the County’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the County’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

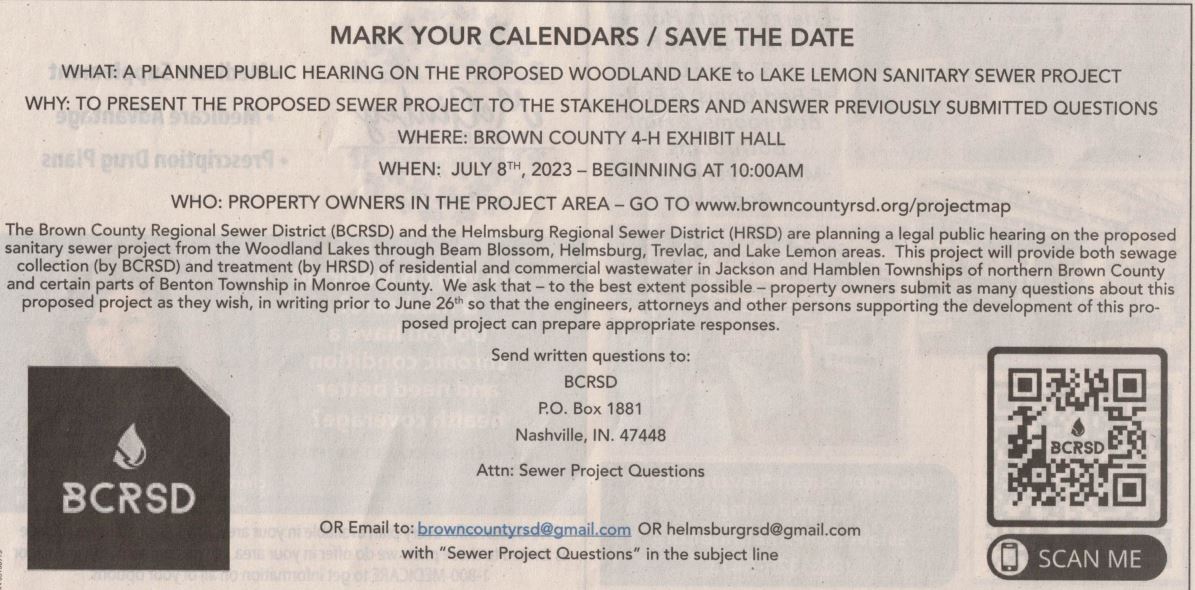

Deadline. The Public Hearing was a required step in the process. The deadline for final comments is July 14, 2023. You can send any comments to BrownCountyRSD@gmail.com or HelmsburgRSD@gmail.com

No Vote at this time – Eastern Corridor. Phase 1 of the project includes a Western Corridor (Helmsburg to Lake Lemon) and an Eastern Corridor (Helmsburg to Bean Blossom to Woodland Lake.). I’ve been following this issue since 2016, routinely attend the BCRSD Board Meetings and have reviewed all of the supporting documentation.

The presentation confirms my previous assessments – the Eastern Corridor should be put on “pause” until the need is validated and there is evidence that the scope of the investment and strategy justifies the expense. It is also important to confirm community-wide support.

In contrast, the Western Corridor has validated the need and has obtained community-wide support.

Despite comments by the BCRSD Board members to the contrary:

“Soils” in Brown County are suitable for septic systems. Soils are tested before a permit is issued.

Impaired “waterways” are not primarily due to waste from failing or inadequate septic systems. Per BCRSDs Watershed Study (pg.63), only 5 of the 22 water samples identified the majority of E.coli as being of human origin. “…pastureland loads more E.coli to Brown County steams than other sources under all modeled septic failure modeling scenarios. Only if 100% of documented septic systems are failing do they contribute a significant volume of E.coli to the entirety of Brown County.” (Watershed study, pg. 69-70)

Community Support? The BCRSD Prelimary Engineer Reports (PER) includes information derived from a taxpayer-funded wastewater strategic plan and watershed study. The plan and study provide the basic premise for the justification of need. The cost of the grant-funded project was $118,000. It required a 10-percent match — $11,800 — which came from the County.

BCRSD Board members refused to hold a public meeting to present their plan. This would have provided them with the opportunity to defend their arguments and conclusions, address questions and concerns and build community support if possible. This should have happened before moving forward with the development of the PER and the Public Hearing. (PER – Read Aheads).

For the Record. I will be asking copies for of all the information submitted by approving officials and will post on Brown County Matters to help ensure responses to all submitted comments and questions were addressed.

Citizenship. American Citizens (top management) have a responsibility to be informed voters and to hold elected and appointed officials (and their contractors) accountable. We also have a responsibility for serving in the role of Jurists to ensure that decisions are based on both sides of an argument. Brown County taxpayers have contributed over a million dollars in support of this project.

Balanced Argument. The presentation at the Public Hearing represents a one-sided closing argument “by the prosecution.” Citizens have the opportunity to provide their input by July 14, 2023. The process requires that responses to be provided by the project sponsors – BCRSD and HRRSD. Approving officials have an obligation to review all the information presented before making a decision. By federal and state statutes, Citizens (unbeknownst to many) do have the right to question or appeal any final decision which should involve a review by subject matter experts that are independent, objective, and represents citizen interests as opposed to those advocating and benefiting from this project. Information from this phase also becomes part of the record.

These government meetings include elected officials and county department heads/employees. The purpose is to discuss issues and concerns within the county government. The meetings, with the support of the commissioners, were initiated by Gary Huett, President of the County Council. The intent was to identify and address issues and concerns and start to build trust. Building trust will require follow-through and changes that will improve results through more effective policies and practices.

Meetings are on the first Thursday of the month, 2:00 pm, Salmon Room, County Office Building

Nov 2, 2023. This was the 6th County Roundtable Meeting. Employees, Council (Huett, Swift-Powdrill, Kirby), Commissioner (Sanders). See link for notes on the previous sessions.

… Unelected 4th commissioner (s)?

Job (Position) Descriptions (PDs)– HR Director and Commissioner Assistant. The PDs are being revised – this will be about the “3rd time” for revisions to the “new” commissioner assistant position.

A Little History on the Positions Drama. Last fall, the commissioners and council determined that a commissioner assistant was not needed. They converted it to an HR Director Position and also funded a part-time receptionist/clerical position. The person that was in the assistant role (Melissa Stinson) left the county to accept a position in Monroe County. In the 2022 primary election, commissioner Biddle, who stated in her campaign that she was the first full-time commissioner in county history, lost in the primary to Ron Sanders. Sanders was elected in Nov. Sanders is not a favorite of the local GOP establishment and is often the lone decenting vote on policy issues being pushed by the local GOP.

Local GOP. The local GOP leadership has the influence to support candidates for council and commissioner who may not have the desire, commitment, or time to devote to their positions. There is a steep learning curve that some may choose not to climb. Thus, having a “full-time” person in the commissioner’s office may be perceived by the local GOP leadership to offer more control over the direction of the county, including “influencing” staffing, personnel, and funding priorities.

HR Director. The HR Director position, it was structured under the theory that the council along with the commissioner’s office and auditor could provide policy and supervisory control over the individual in the position. It was later learned that only the commissioners have supervisory authority. This lack of control over an important position upset some of our elected officials.

New Commissioner Assistant. When Commissioner Braden resigned due to job conflicts, the local GOP on a vote of 7 to 4, elected Blake Wolpert as the interim commissioner. Among his first acts was to take action to re-employ Melissa Stinson – initially as a contractor, while at the same time, creating a new full-time commissioner assistant position. This position was first approved in the absence of a formal commissioner meeting and then approved by the council. It was then learned that the commissioners have sole responsibility for position description and the council only over the pay grade. Despite the budget deficit, the revised PD and pay grade were then updated and approved by the Commissioners and council. The position vacancy was advertised, there were several applications, and Melissa Stinson was hired. Melissa is also the secretary of the local GOP.

The controversy over the assistant commissioner position including the need, roles, and responsibilities were discussed in the previous meetings (see below).

Transparency. I assume the new PDs for the HR Director and Commissioner Assistant will be discussed at the next commissioner meeting where they may take a vote to approve before the public has an opportunity to review the PDs. I suspect that the changes will reflect a shift of more power and control from the HR Director to the commissioner assistant thus allowing the local GOP to restore their influence and serve in the role of an unelected 4th commissioner.

Initial discussions on the PD referenced an administrator role vice assessitant role. An “administrator” would fall with a “professional” category supporting a higher salary grade.

A few years ago, the county experimented with having a full-time “Executive Administator.” This turned out to be problematic and was eliminated.

GOP Monopoly on Power. Note that a one-party monopoly on political power, can PREDICTABLY, lead to the centralization and abuse of power where the special interests can determine policy and funding priorities. The local GOP is led by realtors who understandably, advocate for development (which can pose a conflict of interest), as opposed to the quality of life and cost of living-related priorities.

May 2024 Primary. All 11 Republican precinct chairs will be on the May primary ballot that offers a “referendum” on GOP leadership. Given the winners in the primary will very likely be elected in the Nov general election, cross-over votes by Democrats in the primary can help shape the direction of the county. There will also be two commissioners on the ballot and three council seats. At the county level, issues are not red or blue. Challenges are managing within a budget, roads, bridges, infrastructure, police and fire protection, and the other critical core government functions.

Other Topics

Longevity/Seniority. – Returning Employees. When an employee quits and then is re-hired, should their longevity (seniority) related benefits be restored? T-Be-Determined. .

Budget Questions.

$150K was budgeted for “attrition recovery.” This was unique and explained generally as supporting turnover-related expenses. This would include the training-related cost of hiring a new sheriff deputy. It could also be used to immediately hire a new employee before the previous employee has left.

$2,000K stipend. This was questioned – apprears that it can be used to pay for an employee to attend a government meeting after business hours, For example, the second commissioner meeting of the month is at 6:00 p.m. and council meetings at 6:30 pm.

New Health Insurance Benefit? A proposed new benefit was discussed. Should employees who opted out of the county health insurance plan be provided with a supplement to cover visits to the wellness clinic? It was estimated that this may cost an additional 16-18K a year for up to 20 employees. This could be less expensive to the county than if they opted for a health insurance plan

Oct 5, 2023. This was the 5th meeting of elected officials and department heads/county employees. There were 5 of the 7 councilmen present, no commissioners, and one county employee.

An interesting discussion on the budget. We have about $1.5. to 2 million dollars more in expenses than revenue. About 20% of our budget (5 of 20 million) is spent on the Justice System – that includes the sheriff’s office, Courts, Probation, Corrections et.al. (In Nashville, (population 1,000), the cost of their police Department has been reported to be over over 50% of their budget.)

Of those on probation due to OWI, the majority are from out of the county. This leads to the question as to what percent of the people running afoul of the justice system live in the county as opposed to outside the county?

In addition to justice system-related expenses, the county also finances police and emergency medical support for the State Park. Historical efforts by the county to be reimbursed for this cost has fallen on very deaf ears at the statehouse. Brown County State Park is a cash cow for the state and revenue is shared with the other state parks.

Next Steps – Get through this year’s budget submittal and start working on some improvements. Given the budget challenges this year, the resolution of some issues has led to a little more in-depth understanding and knowledge of finance, accounting, and budgeting challenges.

Overall: An assessment is that the county has about $1.5-2 million dollars of more government than we have the budget to support. This is a hard reality and requires leaders to be more deliberate in spending. Our accounting system can be a challenge in providing needed and timely information.

Salary Grade Structure – An Improvement. Councilman Redding briefed a concept of replacing the 30 pay grades with just a few “Tiers.” It was well received – funding neutral at this point but a change would provide a better foundation for managing payroll, longevity pay, stipends, increases, et.al.

Salary – Market Rates and Turnover – Options? The county is not competitive with pay – especially in the Sheriff’s Department which leads to turnover. An option is a “freeze” where the payroll accumulating as a result of vacant positions can be used to fund the higher pay of existing employees. This leads to the need to re-balance and reduce staffing. Labor costs are always among the highest expense categories in organizations.

Grants. Contracting with grant writers (ARA in Columbus) was seen as an option for getting more money to fund operational costs.

Where does the money go? And how can other counties be paying at much higher levels than Brown County? The common answer is that larger counties have a larger tax base with a more diverse commercial base. Brown County is classified by economists as a Bedroom Community – people choose to live here and commute to jobs outside the county and many can now work from home. We are also a naturally occurring retirement community (NORC). Given this fact, the county opted for a tax policy of high income and low property tax. The low property tax contributed to the demand for land and homes that led to higher prices and homes considered unaffordable at the more modest income levels.

It would be interesting (and time-consuming) to do an analysis of the comparison between counties -ratios would be helpful. Would also need to identify outputs, volumes, etc. Then you could compare things like cost per assessment, per record filed, permits granted, etc.

Some additional facts. On tourism, note this accounts for around 12 million in taxable wages. The total taxable wages for the county is over 425 million (in 2019). The land, terrain, country, and more rural lifestyle, are what has been attracting and retaining residents. The age of poplulation is among the highest in the state and enrollment in schools has been consistently declining since 2009.

Vision? A little déjà vu – employees mentioned the need for a county vision, strategy, new comprehensive plan, and affordable housing. I started looking at these issues in 2016 and a few thousand hours later, have a little understanding of the culture and economics … and a pretty good collection of documentation and research. Up to now, there has not been a demand for any major changes – the status quo has been seen as good enough.

SWOT. In making the case for change/improvement, can start with a SWOT analysis – Strengths, Weaknesses, Opportunities, Threats/Challenges. Opportunities point to solutions that then require the identification of the scope and extent of the problem. Supporting information at https://browncountyleadernetwork.com/

Inefficiencies 20-40% OF Budget? In the quality profession, a general rule of thumb is that inefficient processes, procedures, internal controls, SOPs, etc.,(cost of poor quality – CoPQ) can range from 20-40% of the budget.

Aug 3, 2023 Govt Meeting #3 2-4 pm. These meetings have been moved to one a month – the next one is Sept 7, 2023, 2-4 pm. Some of the issues covered at this meeting were also addressed at the Aug 4 commissioners’ meeting. This post at Brown County Matters.

Main agenda topic was on the compensation (salary) system and the need for a major improvement. Benefits are another important consideration regarding a total compensation system.

Budgets. The counterbalance to total compensation benefits and costs is revenue. When working to develop a new annual budget, the county starts off with a 1 to 1.5 million dollar deficit. This does not include unfunded costs associated with needed repairs and replacement of infrastructure. For instance, there is a need to replace air condition units at the jail at a cost of 640K plus. There is only 75K left in the 3 million capital improvement loan that will be paid off in 2024 at which time a new loan can be obtained. Given increasing interest rates, it is likely that property taxes will have to be increased unless less money is borrowed to keep the rate about the same.

Note that money from the loan was inappropriately applied to cover operating expenses (ambulance contract). The county has not been required to reimburse the fund.

Proposed New Position. A follow-up on the controversy regarding the proposed new commissioner’s assistant position and the job description was not on the agenda and appears to be on the back burner at this point. Two complaints were filed with the state’s public access counselor regarding the process for approving the proposed new position. Employees also raised issues with the need and quality of the job description at the approved pay grade.

New Service Contract. At today’s (Aug 4, 2023) commissioner meeting, a new service contract for Melissa Stinson (former admin assistant). She will be providing as-needed/requested assistance to the commissioners at a rate of $25.00 per hour. She will be receiving a 1099 vs a W2. Commissioners Pittman and Wolpert voted to approve the contract; Sanders was the No vote. The desire for a full-time assistant started with the appointment of Wolpert to the commissioner vacancy as a result of the resignation of Chuck Braden. No detailed explanation as to why a full-time assistant was needed – justification was anecdotal. The invoices should provide the detail as to what specific services are being provided.

2024 is an election year and two of the commissioner positions (Pittman, Wolpert) are on the ballot. Good opportunity for voters to ask the prospective candidates about duties, roles, responsibilities and level of commitment.

Compensation (Salary) System. The county system – well-intentioned, has evolved over time to include “35 grades” and is contributing to conflict and lower morale. The Council is looking to find a better system. Of the 92 counties in Indiana, I would suspect that there may be at least one system that would come close to meeting county requirements. Federal and State governments have figured out the issues and challenges. Appears counties are on their own. Is the State Personnel Department a resource that can be used to provide some advice and support?

Benefits. Part of the compensation package are benefits. The council identified that employer taxes such as FICA and PERF (state retirement systems) add about 18% to salary costs. Health Insurance is also an added cost – counties cost averages about 10K per employee (1.5 million/150 employees). The cost of the clinic and pharmacy can average about 2K per employee (300K/150). Another intangible benefit is job security, holiday/paid leave, and working hours and conditions.

On Health Insurance, the county is self-insured. The employer costs of defined plans available for State employees can be around 7K a year for a single person and 20K for a family. The self-insured option is less expensive but has higher risks if there are a number of serious health issues. Consequently, building up a saving account is imperative – another potential unfunded liability.

Policy – Position Descriptions. A first step in addressing fairness and compensation issues regards position descriptions. For 20+ years (?), the council has been assuming the responsibility to review and approve but it has recently been discovered that position descriptions are a commissioner’s responsibility. The council is responsible for ensuring the appropriate level of funding. An interesting finding – both the commissioners and council pay for legal services and updates of position descriptions have been contracted out to a company that performs this task for other counties. Indicates a weakness in internal controls at many levels.

Internal Controls. Effective internal controls require a review of the statutes that govern an office. You then identify the stated, implied, and essential tasks. Essential tasks are those that if not performed, result in mission failure. Internal control is the checks in place that prevent failure. At the federal level, an annual review of internal controls is required of all agencies including their respective departments and branches. The purpose is to ensure the effective and efficient use of taxpayer dollars.

Note also the process involved in managing internal controls also supports a review of position descriptions. Identification of the tasks supports position classifications.

NEW Position Description Ordinance. At the commissioner’s meeting Aug 4, 2023, a new position description ordinance was proposed. The vote to approve was tabled until the next meeting to allow time for review,.

Note Indiana code “just” requires that citizens be informed of a new ordinance (via legal notices and two meetings) IF it involves a penalty or forfeiture. The septic ordinance fell within this category. (IC Code 36-2-4-8). A second reading can be waived IF there is unanimous consent of the voting members (IC 36-2-4-7).

Position Classification. My question on Job Descriptions regards the process for “classification.” “A classification system groups similar jobs (with like duties, authority, responsibility, and qualifications) into the same position classification so that the same schedule of pay can be equitably applied.” Example – State of IN https://www.in.gov/spd/compensation//

Citizens and employees should have confidence that a job is needed to perform the respective mission of the organization as required by statute, is “independently and objectively classified” and the salary is at the appropriate (and affordable) level.

July 21, 2023.Meeting #2,. The second government meeting (departments, employees, elected officials). The first meeting was on July 7, 2023, from 2-4. One of the strengths in the county is the longevity of many employees, which can bring some context to several issues to include those related to staffing issues.

Topics covered at the first meeting included: Pay, pay comparisons with other counties, county finances, personal administration and policies, health benefits and employee costs, position management, working conditions, culture, policies, procedures, budgets, communication, and county economics. This is expected to be the first of many future meetings. The caution should be that identifying problems without following up with practical and successful solutions can do more harm than good.

I tried to capture as many of the points and issues as I could. I’m sure I missed things or did not capture the sentiment of what was expressed. I did add some of my commentary and links to additional information on the topic.

One of my goals over the next 12-18 months is to develop a “Brown County Fact Book” with sources to help support a fact-based perspective on the county, including economics, culture, jobs by type and industry, employment, demographics, population, tax rates, plans, studies, local politics, et al. I’ve been collecting (and sharing) some of this information since 2016.

July 21, 2023 Meeting.

Council Members in attendance: Huett, Kemp, Kirby, Byrd, Swift-Powdrill (Rudd, Redding absent). Commissioners: Ron Sanders. (Pittman, Wolpert attended the first meeting).

The Hot Topic – in the Long-Run – Compensation – Pay and Benefits. Councilman Kemp identified his observation that pay was not adequate and needs to be increased.

This immediately creates the expectation that changes will be made to address the situation. What was not discussed was how this would be funded. Commentary:

The county is funded primarily by income and property tax. We have to renew a loan (went from 2-3 million) to finance capital improvements (infrastructure). As reinforced at the meetings (and a repeat finding by the SBOA), we have no capital improvement plan and budget but we started working on one. No question that we have unknown and unfunded liabilities. Commissioner Sanders started confirming an inventory of buildings and emerging maintenance issues – for instance, AC unit replacements at the Jail at around 600k.

I’ve been attending commissioners/council meetings since 2016. My take:

The council made a policy decision in the 90’s to keep property taxes low and rely on income taxes. The county income tax doubled in 10 years and maxed out. A couple of years ago, the county shifted from increasing income tax to property tax. BUT, given the constraints of state tax policy, we have been limited to only very minor increases in the property tax rate (determined by a growth quotient).

Changes in property tax bills primarily reflect higher assessments due to market conditions – not as a result of the council increasing the tax rate.

My understanding. The state does not allow a county to max out the income tax rate and then shift and start trying to max out the property tax rate. The county still has among the lowest property tax rates in the state.

In 2018, former Councilman Keith Baker facilitated a meeting by our financial consultant at the time (Umbaugh) to explain the tax policy. Umbaugh and Associates (Now BakerTilly) provided a presentation at the library that illustrated the complexity of our tax system – The Basics of Local Government Budgeting. The information included “scenarios” (pages 22-24) regarding transitioning from the high-income tax rate/low property tax rate option. Good luck trying to understand it but knowledge is needed to understand the options for raising more tax revenue and the respective constraints.

Due to constraints on revenue, former councilman Critser and Baker worked to balance revenue with pay and benefits. This included pay freezes (5 years at one time) and foregoing cost of living increases. Over the past few years, employees have been getting cost of living increases.

Baker led a Salary Study in 2018 that compared employee compensation with other counties of our size – the logic being that counties with a smaller population would have similar financial constraints. In this comparison, Brown County’s compensation was among the best.

The exception in the study was truck drivers with CDLs that were paid more because of the turnover and competition.

This study was criticized by employees that believed their pay should be comparable with surrounding counties and near similar jobs. Higher populations result in higher revenue and bigger budgets. Higher salaries also can increase competition and expected levels of experience and education. Turnover is an indication of non-competitive pay and benefits.

The sheriff’s office recently (2021) justified a pay increase. The cost associated with training deputies and turnover justified the higher salaries. Ref: Deputies’ pay raise request approved by Suzannah Couch –

Discretionary Offices/Department. The two discretionary offices in the budget are the Veterans Office and Parks and Rec. Other offices are required by statute.

2023 Indiana County Income Tax Rates – max is 2.5% that can be increased via a “Growth Quotient.” Brown County’s income rate is frozen at 2.5234%. The highest in the state is:. 2.9% (Wabash)

2023 Property tax Rates by County. Property taxes are assessed by a taxing authority. Brown County shifted from increasing income taxes to property. Increases are limited to the “Growth Factor” determined by the State and given to all counties. The council can vote to accept (they usually do) or reject the increase. Other taxes that be assessed on your property (wheel tax, school referendum other) are listed on your tax bill.

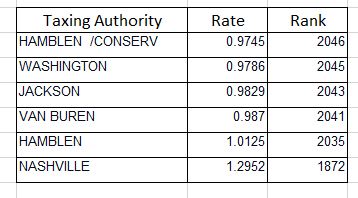

There are 2,080 taxing authorities in Indiana. In Brown County, these townships/conservancy, along with their tax rate and rank, include the following:

The Hot Topic — New Commissioner Assistant Position. The council approved the county commissioner assistant position grade 14 (42k), at their July 17 meeting with votes to approve by Huett, Kemp, Rudd, and Kirby. Darren Byrd, and Judy Swift-Powdrill voted no. Redding abstained (counted as a no vote).’

This topic also came up at the first meeting (July 7) with the expectation that action would be taken to validate the requirement, job description, and pay grade. Concerns were raised that their input was ignored, that the position was over-graded, pre-selected, full of redundancies and inaccuracies, and maybe not needed. Commissioner Sanders wisely declined to comment citing possible litigation. The decision for the new position was made by Commissioners Pittman and Wolpert in the absence of a public meeting.

Note: I filed a complaint with the Public Access Counselor questioning if the decision by two commissioners to create a new position was in violation of open meetings laws. I also filed a complaint questioning the validity of the vote by Councilman Rudd who voted via Zoom.

Pay Grades. The county’s process for determining pay grades has been incremented over time and has resulted in 34-35 pay grades. Information from other counties is being collected to help identify other options to include options for compensating experience. County offers $100.00 a year in longevity pay. So, someone with 10 years of experience compared with a new hire in the same position, would only be making $1,000 more in salary. Job positions also do not e include a range based on level of experience and education. For example, an option could be that a position be advertised at a starting grade of 6 with automatic yearly promotions to a 9.

Job Descriptions and Classification. A surprise at the July 7 meeting was regarding position descriptions. The County contracted with a company to update all the job descriptions and the final versions did not include the input provided by the Departments.

The “So what? “ Job descriptions and classifications provide a baseline for pay and help with pay comparisons with other counties and the private sector. The inaccurate descriptions have led to requests for pay increases to compensate for the new/updated tasks. Once a position or pay is upgraded within one department, most everyone in the other departments may expect that they should also be receiving pay increases as well. An increase in one area starts a cascade which can contribute to lower morale and less trust and confidence in county officials.

Management Culture – Top Down. Another insight was the perception that the overall management culture is dictatorial vs collaborative. Commissioners and Council identify a policy and everyone is expected to fall in line without question. This was interesting and correlates to the perception that major decisions by the council and commissioners are rarely influenced by citizen input.

Pay Comparisons. Pay differences compared with what surrounding counties are paying can be significant. Comparisons require accurate position descriptions.

Health Benefit Costs, Changes in the health insurance benefits had to be made to slow the rising costs (about 2 – 2.5 million a year). This led to higher costs for employees. The clinic is seen as a good feature, but depending on plan options, out-of-pocket expenses can be significant. The county is “self-insured and a few catastrophic illnesses could have devastating financial consequences. The council and commissioners accepted the Risk instead of paying the higher costs associated with defined benefit plans. For instance, at the State, just the “county “cost per employee is around $7,000 for a single person and $20K for a family.

Waste and Inefficiencies. Areas identified as potential improvement were in using consultants as opposed to using/developing internal expertise for a variety of studies, plans, and project contracting practices. It was also identified that new positions were created that included tasks that were previously routinely being done one or more by others.

Performance Reporting. It was mentioned that one time, some departments would brief (or want to) their contributions at least once a year but the process was not encouraged or sustained.

Commentary. Each Department briefs its proposed annual budget. Adding in accomplishments from the previous year might be informative. Adding the review of performance and accomplishments as an agenda item at a commissioners/council meeting may also be helpful in building community trust and confidence in their local government.

New Source of Government Revenue? It was mentioned that the Music Center is having a good year. Any “excess profits” can be returned to the county as opposed to 75% (if legal) donated to the Brown County Community Foundation. The Innkeepers tax is a county asset and managed by the county that was used as collateral for the loan to build the Music Center. It can be used for just about anything that supports tourism.

Cost of Living – Affordable Housing. The county tax policy of low property tax has contributed to the high demand for land/housing, tourist-related businesses, and higher prices that have led to Brown County’s high median home values.

Bedroom Community. Ball State economists have identified Brown County as a bedroom community – people live here and earn their income outside the county. The majority of workers still commute to jobs outside the county (statsIndiana). We have also become a Natural Recurring Retirement Community (NORC).

The Brown County Community Readiness Initiative, a survey and economic assessment conducted by the Ball State Economic and Research Institute, concluded that Brown County’s greatest potential for economic growth is not tourism, but as a bedroom community. – BC Democrat – Sara Clifford

Population Projections 2020-2050. Brown County’s population is expected to decline and student enrollment has been declining since 2009.

Available Land. The fact that more than half our land mass is owned by the state and feds is seen as a detractor. However, it is also what attracts and retains new residents.

Brown County’s Economic Engine? Tourism brings in 12 million in taxable wages. Total taxable income by everyone that filed a state tax return was over $524 million.

Expansion of Sewers and Economic Development? Brown County has among the highest median home values in the State, supported by lower property taxes. Consequently, homes are no longer affordable at modest to lower income levels. Expanding sewers “may” lead to more housing but given market demand, prices may not be at the modest end of the affordability range. The Brown County Comprehensive Plan (PDF) does not identify higher-density apartment options as a desired option.

Individual Performance Evaluation / Feedback. This can be a debatable issue. Individuals work within a system. The system determines the majority if not all of the result. Assessing the performance of the system is a good thing. Assessing individuals within the system can be problematic. Individuals and groups can choose to assess their strengths and weaknesses and improve goals that would contribute to improvements in the system.

For example, Grades in school can do more harm than good. Children control very little of the variable that affects performance. An article on the topics: — Are-grades-effective-and-fair?

Commentary — Some Ideas – Organizations – Groups

What is your purpose? Identify the Mission and Functions (tasks) for every organization. Can post these on the website. Plenty of examples from other counties?

Why do you exist? What is the link to governing statutes and regulations?

What are the mission-critical tasks – that if not done, result in mission failure?

What are theinternal controls (checks) that you must have in place and follow to prevent mission failure?

What do you provide? Identify the services produced or provided, e.g., the outputs and the volume.

How well do you do perform your mission? Assess organizational performance

What’s changed? Periodically review job descriptions, classifications, missions and functions, and performance.

The Brown County Leader Network offers a self-help guide for supporting continuous improvement. Addressing issues included in the meetings can start with SWOT analysis.

The County Council determines the amount of property taxes that will be needed in order to fund the county government. 2024 Budget Hearings: August 15,16, 17 at 5:00 p.m.

Aug 17, 2023, Meeting 3 of 3. Budget Hearings – 2024. All the proposed budgets from the department have been submitted. Council has a lot of work to do to complete the 2024 budget. The final county budget hearing is scheduled for Sept 18, 2023. It is due to the State by Oct 31.

Convention Visitors Commission (CVC). I routinely challenge the CVC budget and lack of oversight by the council. The CVC manages the revenue from the innkeeper’s tax. The revenue is a county asset. Revenue from the tax was pledged as collateral for the loan to build the BC Music Center (BCMC). It is also shared with the Convention Visitors Bureau (CVB) which is responsible for tourism-related marketing and promotion. The revenue from the tax can be spent on just about anything that promotes tourism.

Similar to the Jail, a separate building corp was established to manage the building. A management group was established to manage the venue. This management group includes a representative from the council (Darren Byrd) and the board of commissioners (Jerry Pittman).

The purpose of creating a separate building corp was so that the debt could be associated with the building corp and not constrain the amount of money a county can borrow. The county still has responsibility for the venue.

The BCMC Admin agreement states that 75% of any excess profits (“if legal”) will be donated to the Community Foundation and 25% to the county taxpayer. Why shouldn’t 100% of any excess profits be returned to the county? This could be used to fund infrastructure-related needs such as roads and bridges.

Is the 75/25 arrangement legal? Was this agreement voted on at a council and commissioner meeting? I do not recall a formal vote on the topic.

By statute, the county council is responsible for reviewing and approving the CVC budget. The expected amount of revenue in 2024 is estimated at 1.3. million. The budget includes 3 line items. Is a 3 line budget sufficient to ensure the revenue from the innkeeper’s tax is leveraged to achieve the greatest benefit to county taxpayers? 2024 CVC Budget

Aug 16, 2023 – Meeting 2 – Budget Hearing – 2024. This was the second of three meetings. The last one is tonight, Aug 17, with the final budget hearing scheduled for the Sept 18th Council meeting. The final budget is due to be submitted to the State by Oct 31. Interesting that if this deadline is not met, the prior year’s budget is used. A small team will be working to resolve the budget challenges within the next few weeks.

Consultants. The council has the responsibility for the county budget. The county uses three consultants – Jacque Clements, Association of Indiana Counties (Council), Baker-Tilly (Commissioners) and Melissa Stinson on contract this year to help commissioners put together their budget. Stinson gets support from both Jacque and Baker-Tilly.

Budget Worksheet. Jacque provides a budget worksheet that is the starting point for developing the budget. This year, it is a “Draft” due to incomplete information. It identifies a shortfall of $54,310 which is not accurate. Councilman Kemp pointed out the likely shortfall in Health Insurance costs at $1.1 million which reinforced the need for budget cuts. Also not included are costs to repair/replace needed infrastructure – such as one or more air conditioning units at the jail at a total cost of 640K plus.

The overall budget system/processes? Pretty sad. Good people working in a bad system that have opted to remain in firefighting mode that has become the status quo – “the way we always do things around here.” This includes a short-term perspective with the priority being just getting next years budget submitted and dealing with the challenges one fire at a time.

Rainy Day Fund. (County savings account). Interesting that Jacque mentioned she works with a county that has 9 million in the rainy day fund. She also mentioned that Brown County has had years with only a few hundred budgeted in the rainy day fund.

Crisis yet? Changing systems like this typically requires a crisis. This could include a situation where expenses exceed available revenue to the point the county has to take out a loan to pay the bills. Further, one can’t have a good budget without a viable strategy and plan.

Contributing to the problem is our one-party monopoly on political power where preserving the status quo takes precedence over effectiveness and efficiency.

Planning – a dirty word? For some reason, the Brown County culture has perceived a plan as a virus to be avoided. A simple thing like a capital improvement plan and budget has been avoided at all costs. Thankfully, new commissioner Ron Sander has taken on this task. He started with getting a list of the properties that the county is insuring. This provides a starting inventory for helping to identify expected repair and maintenance costs. For instance, the prosecutor’s office has been on the “talked-about” list for a replacement for years. Replacement may be a priority for the next capital improvement loan in 2025. We only have 75K left on the current loan.

Finance and Budget Information. The State does not make it easy for any citizen (and elected official) to learn about State/County finance and budgeting. Consequently, this leads to the need to rely on consultants. It also requires a longer learning curves for government officials. And, you have to have a desire to learn a foreign language and few may be willing to put in the time needed to overcome the learning curve. The Budget Worksheet illustrates the point.

Aug 15, 2023. Meeting 1 Budget hearing – 2024. This was the first of 3 initial budget hearings.

Tax Increases. The county’s budget consultant was not at this meeting. The consultant identifies the projected deficit and the percent/amount of property taxes the council can choose to raise via a growth quotient. The growth quotient is 4% this year or around 200k. The council must vote to accept or reject the increase. The council routinely votes to accept. Council has also routinely approved a 3% cost of living raise for employees. In the past, the 3% was estimated to cost around 130K which leaves 70K of “new” revenue.

Balanced Budget? The projected “net new revenue” is not enough to fund the county. In order to balance the budget, we routinely understate expenses. What we do not do and should do is identify what we know to be unfunded liabilities. This lack of due diligence caught up to this year when the council and commissioners had to scramble to find funding for both health insurance costs and funding a new addition to the courthouse.

On tax policy, the county opted to rely on revenue from income taxes vs property taxes. We maxed out on income tax increases and shifted to relying on the growth quotient from assessed property values

Property taxes can also be raised to fiancé debt. We routinely have been borrowing money to fund infrastructure costs. The recurring debt from a loan increased from 2 million to 3 million and there is only about 75K remaining on the last loan that expires in 2024. Over 600K has been identified as being needed to replace air conditioning units at the jail.

Longer-Term planning? The county’s budget process is typically focused on the short-term, e.g., the next year. No long-term goals for savings, investments, and spending priorities. On spending priorities, a capital improvement plan and budget is finally starting to be developed. The lack of a plan was a repeat finding by the State Board of Accounts that was routinely ignored by county officials.

Financial Plan and Strategy? We have had a Financial Plan that was not integrated into an overall finance and budget plan and strategy. A published financial plan reportedly helps the county to obtain a lower-interest loan. A recommended goal for counties is to maintain at least a 15% balance in major fund accounts. Should not be too difficult to track the status of such a basic goal.

Description: The county receives an estimate of revenue for 2024. This includes what will be allowed as a tax increase if approved by the council.

Departments – using their prior year histories as a baseline, identify expenses. A review is conducted to balance revenue and expenses. State reviews and approves the budget and publishes the budget order in January.

Surprises. The area of surprise is the renewal of contracts and the unfunded requirement for repairs and replacement of infrastructure.

What’s Missing? At least an annual review of budget performance which would include actual expenses vs planned and planned savings vs projected savings would be helpful. The goal is a minimum of a 15% fund balance. Some counties have savings in a Rainy Day Fund that will cover a year’s worth of expenses.

Contract Support

Jacque Clements, Association of Indiana Counties.

Services to be provided by Melissa Stinson – former commissioner admin assistant. (RFI submitted on July 6, 2023, for a copy of the contract)

Caitlin Cheek, BakerTilly

Additional Information – FYI

Outline – Baker-Tilly – Proposal – Scope of Work – Budget Support – Overall Context

A. Annual Budget Assistance and Analysis (Consulting Services)

Meet with the Client to discuss the budget process and collect data for budget preparation.

Develop or analyze the budget calendar for consideration by the legislative body.

Assist with Client prepared budget estimates.

Compute state-distributed revenues based on formula sheets, certifications, and other information provided by the Department of Local Government Finance (“DLGF”) and the Auditor of State.

Compute miscellaneous revenues based on historical information provided by the Client.

Compute the estimated maximum levy.

Compute the estimated tax rate and levy by fund.

Assist with the preparation of prescribed forms related to the annual budget.

Assist the Client with entering budget data into the Indiana Gateway program.

Monitor the completion of the required steps of the budget process with the Client.

Attend public meetings at the discretion of the Client to present budget information to the legislative body.

Analyze the 1782 Budget Notice on behalf of the Client to ensure accuracy and completeness.

Provide periodic budget management assistance through telephone, remote and on-site support.

B. Levy Appeals (Consulting Services) (as necessary)

Assist the Client with determining its eligibility to apply for a property tax levy appeal with the DLGF.

Assist with the preparation of the State appeal application and supporting documentation for levy appeals.

Submit the levy appeal petition and application to the DLGF.

Monitor the completion of the required steps of the levy appeal process with the Client.

C. Additional Appropriations (Consulting Services)

Develop a timeline for the steps required to request approval of an additional appropriation from the DLGF.

Analyze estimated receipts and cash on hand to determine ability to fund requested additional appropriation.

Assist with State prescribed additional appropriation documents.

Assist the Client to monitor completion of the required steps of the additional appropriation process.

D. Reestablishment of Cumulative Fund Rate

Develop a timeline for the steps required to reestablish the rate on the Client’s cumulative fund.

Preparation of State required documents.

Preparation of the notice to taxpayers and establishing ordinance for local counsel review.

Attend a public meeting, as requested, to discuss the establishing process and the estimated revenues to be generated from the tax rate.

Additional meetings are covered under Section E below.

Assist the Client to monitor completion of required steps of the process.

E. Other Accounting and Required Support Services (Consulting Services)

Analyze historical financial information and develop estimated financial reports and analysis.

Attend other meetings not covered under the Scope Appendix above.

Provide other required accounting support services.

Meeting Changes. Commissioner meeting; Aug 16 meeting will be at 2:00 vs 6:00. (conflict with budget hearings). Wed Aug 2 meeting time changed to Fri Aug 6 at 2:00.

Council Meeting. Per a legal notice in the Democrat, the council will be having a meeting this Friday, July 7, from 2-4.

Budget Hearings – 2024 Elections. Hearings scheduled for Aug 15,16, 17 at 5:00 p.m. Suggest all candidates for office in 2024 attend ALL of the meetings.

Salt Creek Trail. The section from the State Park to the Red Barn may be paved within the next few weeks – weather permitting. There is no longer a financial commitment from the Feds/State on funding to connect the trail from the YMCA to the Red Barn. And, an easement to cross the property crossing the Red Barn / Hesitation Point Pottery is needed.

Interesting Commissioner Dynamics. Ron Sanders brings some needed perspectives and challenges to how “this is the way we always do things around here” which leads to some friction. Challenges to any status quo are predictably unwelcome in most cases. Sanders defeated the local party’s preferred candidate in the primaries which has most likely contributed to unwarranted friction including from party officials and loyalists serving as trolls at meetings. Sanders was elected with over 3,000 citizens and any perceived disrespect shown to Sanders also indicates contempt for his voters that may not be aware or happy with what may be going on.

One noticeable improvement is that Sanders reads the contracts and ensures that the legal council reviews them before the vote to approve. This prevents the county from being liable for unnecessary costs and risks. He also reinforced that some claims need to be provided to the commissioner five days in advance to include verification of required documentation. This requires the cooperation of ALL departments including the commissioner’s office. He also pointed out the need for a review of minutes by ALL the commissioners in addition to the auditor’s office.

Note: I personally haven’t agreed with a few of Sander’s votes. He identifies his rationale and is open to challenges and changing his mind. Welcome to America – where people can still respectively disagree. And Kudo’s to Commissioner Pittman for always keeping a calm demeanor, reinforcing the need for cooperation, and admitting to mistakes – rare qualities. We also have amicably shared disagreements on a few decisions.

Political Culture and Risk to Citizens. We have a one-party monopoly on political power which almost never produces the best behavior, decisions, and results. In a political monopoly, good people get caught up in a bad system that undermines their potential, character, talents, contributions, and sense of morality. Monopolies’ desire to centralize power contributes to a culture that can lead to no competition on ideas and no debate or analysis regarding proposed solutions. Note that Citizens are responsible for serving in the role of “Jurists” to ensure both sides of the argument are debated and analyzed before a decision is made. Decisions should be supported with documentation that supports the aim of a balanced argument.

NEW Commissioner Administrative Assistant. Well, this was interesting and included references to the psychic hotline – a first. Ron Sanders asked about a job posting for a full-time commissioner admin assistant on the county website. Appears two (?) commissioners (in the absence of the required public meeting), may have agreed to a new position that was posted to the county website. If a new position is a SOLUTION what is the PROBLEM? Historically, commissioners just had ONE administrative assistant. Commissioner Pittman acknowledged posting the announcement was a mistake and Commissioner Wolpert (recently appointed) stated he knew nothing about it and commented that the allegation was a psychic delusion. This caught my attention. I reinforced that the announcement was on the county website and I shared it on Matters. It was removed before the meeting. In the spirit of satire, I did check – no reference on the website or a toll-free number regarding psychic advice.

In the more drama category, the council needs to approve any new job and provide funding. Neither of these steps was done. Further, the council last year (post-election?), with no pushback from commissioners, changed the original job description of the admin assistant to an HR Director and approved a part-time commissioner assistant. Plus, the council attempted to insert themselves into a supervisory role over the HR director contrary to state law.

As Ron Sanders pointed out with the confirmation by legal, supervisory, and related responsibilities is a commissioner – not a council, responsibility. AND, like this is not enough, the context for identifying a desire and then posting a new position ”creates the perception” that the new position may represent a favor for a political loyalist. Commissioner Pittman reinforced that if/when funded, the required steps will be followed to ensure the best candidate is selected. Commissioner Pittman’s 2nd term ends in 2024.

However, before a new position may be created, a good case needs to be made that an additional position is actually needed. For instance, the former commissioner alleged that she was the first full-time commissioner in county history. This infers that it required her to spend full time on part-time responsibilities and/or, the other commissioners were not contributing to the workload and/or the overall commissioner workload has increased significantly beyond historical norms. An analysis of the need for a new and full-time admin assistant should include identifying tasks, outputs, and responsibilities and perhaps benchmarking with other counties.

In context for the potential of moral and political corruption, the worse case for citizens is to have a full-time administrator (or executive) beholden to the direction determined by party officials. This along with expecting that some elected and appointed officials perform as expected and everyone else should get on board is not a good thing for a republic. Preventing the potential for this level of corruption requires the due diligence of citizens and candidates for office that will serve everyone and not just the few that are too easily addicted to power and froth at the mouth when they can wield power in making decisions that can affect thousands of people.

Budget Support Contract. The contract with the former commissioner admin assistant – Melissa Stinson, was approved. This had the support of Pittman and the advocacy of Wolpert. Sanders voted No and suggested using Baker-Tilly. I’ve requested a copy of the contract and will be asking for expense reports (public information). This information may be useful as a benchmark in preparing the budget for 2025. On budget preparation, in the past, former commissioner Biddle prepared the commissioner’s budget. The overall process underreports costs such as health benefits and unfunded requirements related to infrastructure repairs and replacements. Note to balance the budget, a former long-term council member stated that revenue and expenses were generally underreported every very year but things tended to work out. This practice caught up to us when our recurring loan had to be increased from 2 million to 3 to cover expenses.

Currently, we have an unfunded requirement to replace air conditioning units in the jail at around a total cost of 600K. (11 units at 55K per, not counting shipping and installation). This expense was identified in a commissioner meeting in “March 2022.” Budget challenges this year required the help of Baker-Tilly to find (over a million) of needed revenue. At last year’s budget hearing, over a million was identified as a shortfall. HINT: This indicates a need for a “systemic” improvement in our budget process.

After inspecting the building (jail) roof and air conditioner units, Sanders identified that more routine maintenance is needed to help keep the units operating at efficiently as possible.

In the quality management area, it is generally understood that systems and processes determine most if not all of the results. A systemic approach to improvement is included in the information provided at the Brown County Leader Network. I have and do plan on volunteering support for budget-related improvements.

Our second President John Adams said, “It (July 4th) ought to be commemorated as the day of deliverance by solemn acts of devotion to God Almighty. “It ought to be solemnized with pomp and parade, with shows, games, sports, guns, bells, bonfires, and illuminations, from one end of this continent to the other, from this time forward forever more.”

The design of our system was influenced by the works of the great philosophers including the Judeo- Christian philosophies that integrated a deep insight into human nature and its tendency to self-destruct. The design included the needed checks and balances on power at all levels of government that have been eroded over time contributing to the divisiveness in America.

Thie divisiveness has been described as spiritual warfare. Spiritual warfare represents the conflict regarding the basis for determining right and wrong – who or what serves as the moral authority? Should it be the modern man that believes that self-government is a quaint concept and should be replaced by experts or elites through more centralization of power? This aim is supported by dividing people by race, gender, age, and culture with a belief that despite the lessons from history, the change will eventually lead to their vision of utopia? Or, do we go “Back to the Future” to re-discover and restore our foundational beliefs and principles that are integrated into the original design of our Constitution?

Power Corrupts. Note that at the local level, Brown County has a monopoly on political power where a few can dictate what they believe is best for the many. Power always corrupts and this centralization of power can never produce the best results. This can also lead to the moral corruption (usually unbeknownst to them) of those that work within this system. Transparency is the best counter-strategy and can start as simply posting Agendas, Minutes, and Audio of county government meetings. The “Minutes” identify what is or has been accomplished. Accomplishments should be the basis for assessing the performance of elected and appointed officials.

Current example – Abuse of Power – Sewer Expansion. A county wastewater strategic plan was contracted for development by “appointed officials” to the Brown County Regional Sewer District (BCRSD) Board without any guidance or input provided by elected officials at a public meeting. The plan was also approved without any public meetings and is supporting an application for “Phase 1″ of a $50.5 million dollar project. The required (by the State) Public Hearing is July 8, 2023.

The County Comprehensive Plan which is the responsibility of the commissioners, is the legal document that should identify what the citizens want and do not want in terms of quality of life, infrastructure, and development. Development of this plan DOES require input from citizens at public meetings.

The aim of our system as identified in the Preamble to the Constitution, is to work towards “a more perfect Union.” The concept of “perfect” is biblically based with perfect described as “all” human needs being met. The underlying belief is that action motivated by love leads to outcomes where everyone can benefit, or at least, not be any worse off. As legendary coach Vince Lombardi, reinforced, “Perfection is not attainable, but if we chase perfection we can catch excellence.”

How do we catch excellence? The secular quality profession has validated through the Taguchi Loss Function, that the closer any action such as the production of a product or service, gets to the ideal of more perfect, the higher the quality and the lower the cost to the individual and society.

Why is continuous improvement a moral imperative? When an action results in more needs being met, there is less harm to some when their needs are not being met. In other words, continually reducing crime leads to fewer victims. Improvement and increased access to health care can lead to less sickness and death.

The basics of continuous improvement? When proposing an improvement, identify everyone (all stakeholders) in the near, mid, and long term that will be affected by the change. This includes identifying their needs, what will be provided, their expectations, and the feedback they need to determine if the change resulted in improvement. Think of citizens as members of a “jury” that needs to see both sides of the argument before making a decision and will be following up to learn if the change produced the desired results

A Way Ahead. The methods and tools supporting continuous improvement towards that more perfect Union (and county) supported by the citizenry have not found its way into government – yet. The basic principles of the approach have been introduced by the Brown County Leader Network.

Brown County author, historian, and cultural commentator Hank Swain (1918-2014) commented that a good idea in Brown County can take about 8 years to catch on. Quality improvement-related strategies tend to take a little longer. Needed improvements at the local level can have regional and national-level impacts.

The required Legal Notice for the Public Hearing was published in the June 21 issue of the Democrat. Questions and comments will be addressed at the July 8 Hearing, starting at 10am, at the 4H Fairgrounds.

Written comments and questions can also be provided through July 14, 2023. Email is BrownCounty RSD@gmail.com.

BCRSD BOARD MEMBERS: Mike Leggins (President), Clint Studabaker (Vice President), Phil LeBlanc ( Treasurer), Richard Hall ( Secretary), Matt Hanlon (At large).

Image by Gary Varvel at

Image by Gary Varvel at

{kind=link}